<b>Marcotullio<b>, P. J., L. Bruhwiler, S. Davis, J. Engel-Cox, J. Field, C. Gately, K. R. Gurney, D. M. Kammen, E. McGlynn, J. McMahon, W. R. Morrow, III, I. B. Ocko, and R. Torrie, 2018: Chapter 3: Energy systems. In Second State of the Carbon Cycle Report (SOCCR2): A Sustained Assessment Report [Cavallaro, N., G. Shrestha, R. Birdsey, M. A. Mayes, R. G. Najjar, S. C. Reed, P. Romero-Lankao, and Z. Zhu (eds.)]. U.S. Global Change Research Program, Washington, DC, USA, pp. 110-188, https://doi.org/10.7930/SOCCR2.2018.Ch3.

Energy Systems

The future outlook for the North American energy system is based on scenario analyses. Scholars have argued that scenarios are a good tool to analyze future trends while addressing uncertainties (Peterson et al., 2003; Schoemaker 1991; van Vliet and Kok 2015; van’t Klooster and van Asselt 2011). Several different approaches to scenario development exist, however (Amer et al., 2013; Börjeson et al., 2006; van Notten et al., 2003). While there are no consensus universal typologies, the review literature often includes three distinct types of scenarios: predictive, exploratory, and backcasting scenarios. This section describes these different scenario types, discusses the advantages and disadvantages of each approach, and reviews scenario results applied or related to the North American energy system and GHG futures. The scenarios reviewed provide information on energy and GHG predictions based on historical and current policies, the future range of plausible outcomes defined by variations in energy and emissions drivers, and the costs of mitigating carbon emissions to create average global temperature increases of not more than 2°C.

3.8.1 Energy and Carbon Emissions Forecasts

Predictive scenarios comprise two different types—forecasts that address how the future will unfold, based on likely development patterns and “what if” scenarios that respond to changes in specified events or conditions (Börjeson et al., 2006). Forecasts typically provide a reference case result that may be accompanied by outcomes of high- and low-type scenarios, indicating a span of options. Sometimes probabilities are employed in attempts to estimate likelihoods of outcomes. Predictive scenarios are useful to stakeholders for addressing foreseeable challenges and opportunities and can increase the awareness of problems that are likely to arise if specific conditions are fulfilled. This type of scenario attempts to answer the question, what will happen? (Quist 2013).

An important criticism of predictive scenarios is that they have a self-fulfilling nature resulting from assumptions of continuity based on past and current trends. Predictive scenarios are based on historical data that define the trends and model parameters that do not change over the course of the scenario timescale (i.e., no policy changes are identified initially), preventing the possibility of transformational changes.

The forecasts examined here include national future projections of CO2e for Canada (ECCC 2016c), the United States (EIA 2017k), and Mexico (IEA 2016b). Each projection set includes a reference case and a defined set of high- and low-emissions scenarios. In all cases, the figures are modeled as projections of “what if” forecasts, given certain assumptions about drivers. The methods and assumptions among the projections presented are neither standardized nor bias-corrected. Despite uncertainties in combining figures, these aggregate national projections are useful in signaling the variety of potential futures for North American energy system emissions.

In its Annual Energy Outlook, EIA (2017k) provides a “Reference” case projection as a business-as-usual trend estimate, given known technology and technological and demographic trends. It generally assumes that current laws and regulations affecting the energy sector, including sunset dates for laws that have them, are unchanged throughout the projection period. The potential impacts of proposed legislation, regulations, and standards are not reflected in this reference case. The cases of “High emissions” and “Low emissions” are based on different assumptions of macroeconomic growth, world oil prices, technological progress, and energy policies. “High emissions” cases include scenarios with high economic growth and those without the U.S. Clean Power Plan (CPP). “Low emissions” cases include scenarios with low economic growth and those with CPP. All projections are based on results from EIA’s National Energy Modeling System (NEMS). The EIA (2017c) “Reference” case assumes that current laws and regulations remain in effect through 2040 and that CPP is implemented. The “Reference” without CPP case is the “High emissions” scenario and has similar basic assumptions to the “Reference” case, but it assumes high economic growth and no implementation of a federal carbon-reduction program. The “Low emissions” case is the low economic growth scenario and assumes GDP annual growth at 1.6% (compared with a 2.2% reference case).

The U.S. “High emissions” scenario projects an increase in emissions of 0.7% (10.4 Tg C) from 2015 to 2040, while the “Low emissions” scenario projects a decrease in emissions of 12.2% (175.3 Tg C) during this period. Across the three presented alternative cases, total energy-related CO2e emissions in 2040 vary by more than 185.5 Tg C (14% of the “Reference” case emissions in 2040). The “Reference” case projects a decrease of emissions by 7.2% from 2015 to 2040, translating into a decrease of 103.9 Tg C. The U.S “Low emissions” case translates into an emissions reduction about equal to the current size of Canada’s total energy-related emissions. Note, however, that even with the low-growth emissions case, the U.S. energy system would not meet the target of reducing emissions by 26% to 28% below 2005 levels (1,640 Tg C) by 2025 (a drop of 426 Tg C and 469 Tg C, respectively), previously proposed in the U.S. INDC (The Record 2016).15 Although the United States has stated an intent to withdraw from the Paris Agreement, this comparison illustrates the kind of reductions needed to meet the goals of the United Nations Framework Convention on Climate Change (UNFCCC) 21st Conference of the Parties (COP21). Note that even if all signatories of the Paris Agreement met their reduction goals, it is unclear whether global temperature increases would be kept below an average temperature increase of 1.5°C above preindustrial levels (Clémonçon 2016; Rogelj et al., 2016, 2018; Obersteiner et al., 2018).

Canada’s energy-related CO2e emissions projections are published by ECCC (2016c) and derived from a series of plausible assumptions regarding, among others, population and economic growth, prices, energy demand and supply, and the evolution of energy-efficiency technologies. The projections also assume no further governmental actions to address GHG emissions beyond those already in place as of September 2015. In the Canadian projections, the “Reference” scenario represents the midrange levels for economic growth (1.5% to 2.2% GDP growth rates per year), stable population growth (1.1% to 1.3%), and slight increases in energy prices, among other factors. The “High emissions” scenario includes high GDP annual growth rates (1.3% to 2.7%) and high energy prices, among other factors. The “Low emissions” scenario includes assumptions of low GDP annual growth (0.8% to 1.5%) annually and low energy prices. Environment and Climate Change Canada uses the Energy, Emissions and Economy Model for Canada (E3MC; ECCC 2016c). Canadian emissions from stationary combustion and fugitive sources, transportation, and industrial processes are presented; emissions from agriculture and waste are excluded. Also, the Canadian projections are for the years up to 2030. The 2030 figures are used here for the 2040 North American analysis.

In the Canadian “Reference” case, Canada’s energy-related emissions by 2030 are 180 Tg C, an increase of 3.6% from 2015 levels. The “High emissions” scenario projects 193 Tg C levels by 2030 (an increase of 10.8% from 2015 levels). The “Low emissions” case projects 168 Tg C by 2030 (a decrease of 3.6% from 2015 levels). The range in emissions represents 14% of the reference case emissions in 2030. Also note that for Canada, in the “Low emissions” scenario, the nation’s energy system would meet its Nationally Determined Contribution (NDC) target of 142.64 Tg C by 2030 (ECCC 2017a).

IEA (2016b) recently provided projections for Mexico under a variety of scenarios. The IEA analysis includes five different scenarios: “New Policies,” “Current Policies,” “450 Scenario,” “No Reform,” and “Enhanced Growth.” The “New Policies” scenario reflects the way governments envision their energy sectors developing over the coming decades. Its starting point is the policies and measures that are already in place, but it also takes into account, in full or in part, the aims, targets, and intentions that have been announced. “Current Policies” depicts national energy system growth without implementation of any new policies or measures beyond those already supported by specific implementing measures in place as of mid-2016. No allowance is made for additional implementing measures or changes in policy beyond this point, except when current measures are specifically time-bound to expire. The “450 Scenario” is the decarbonization strategy, which has the objective of limiting the average global temperature increase in 2100 to 2°C above preindustrial levels. The “No Reform” case is an illustrative counterfactual case that deliberately seeks to portray what might have happened to Mexico in the absence of its energy reform initiative announced in 2013. Finally, “Enhanced Growth” uses a higher assumption of GDP. This chapter identifies the reference case as the “New Policies” scenario, “Current Policies” is the high-emissions case, and the low-emissions case is the “450 Scenario.”

Among these scenarios, changes in Mexican CO2 emissions from 2014 to 2040 range by 50%. The reference case (“New Policies”) projects an increase in emissions from 118 to 124 Tg C (5.6% increase) during the period. The high-emissions case (“Current Policies”) projects an increase in emissions from 118 to 140 Tg C (19% increase). Alternatively, the low-emissions case (“450 Scenario”) projects a decrease of almost 34%, with levels in 2040 reaching 78 Tg C. With the 450 Scenario, Mexico still will not meet its NDC target of reducing unconditionally 25% of its GHG emissions (below the business-as-usual scenario) for the year 2030. That is, the required 25% of the business-as-usual case (i.e., reference scenario) is a reduction of 29.3 Tg C (or 25% of 117 Tg C), but the reduction by 2030 using the 450 Scenario is 20 Tg C (117 to 97 Tg C). Again, these projections demonstrate the difficulty of meeting targets set forth by the Paris Agreement.

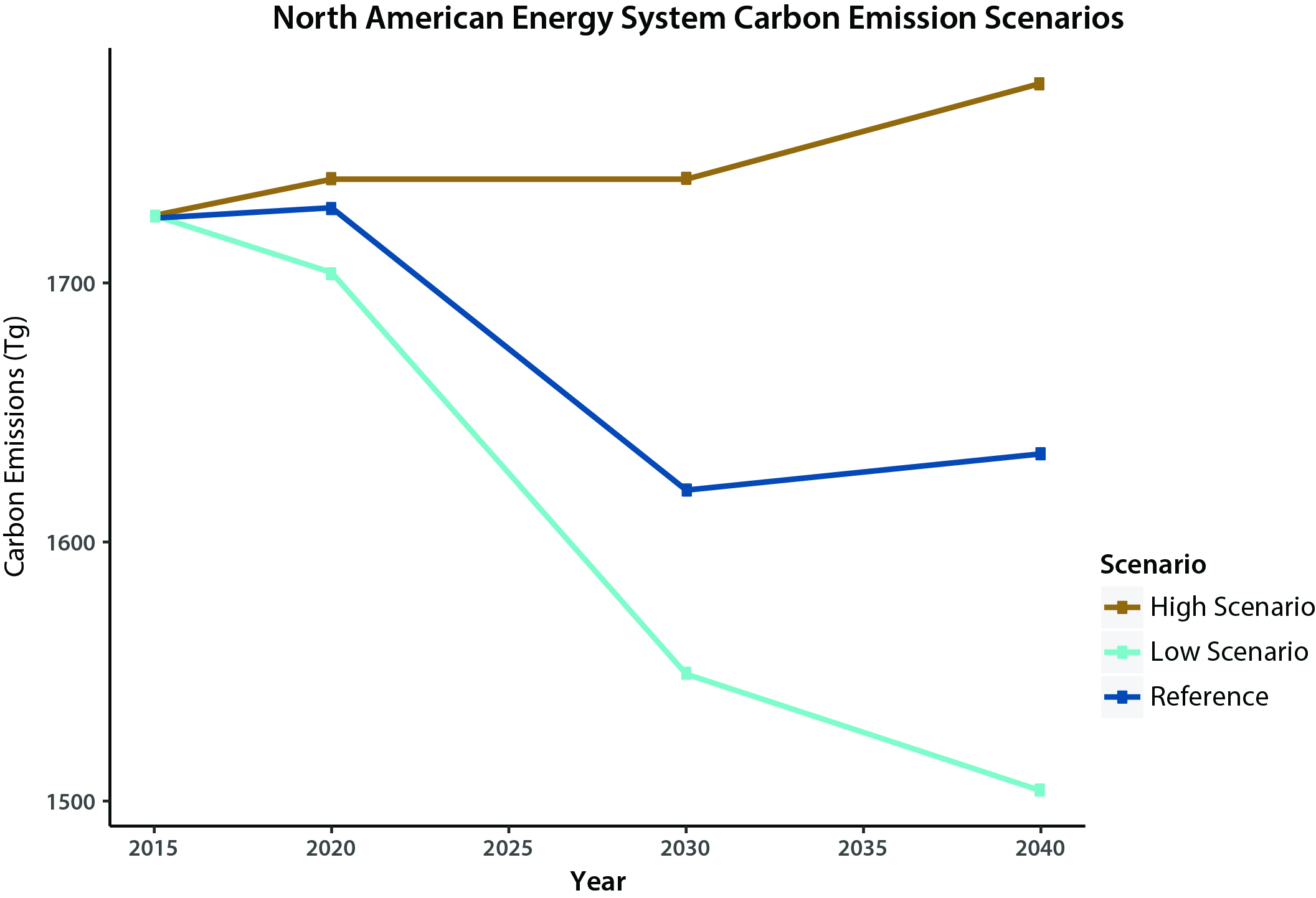

In aggregate, the data from these various models project future North American energy-sector emissions ranging from 3.0% higher than 2015 levels to 12.8% lower than 2015 levels by 2040 (see Figure 3.11 and Table 3.5). The aggregate “Reference” cases project a total 5.3% decrease in emissions from around 2015 by 2040. To ascertain a sense of uncertainty of these figures, the range of emissions from this set of projections is compared with regional estimates from private-sector forecasts of BP (2016) and ExxonMobil (2017), along with those of IEA (2016a). Both BP (2017a) and ExxonMobil (2017) project decreases in North American emissions. ExxonMobil (2017) projections, which include only the United States and Canada, suggest a 14.5% decrease in emissions by 2040 compared with 2015 levels, while BP (2017a) projections, which include all three nations, suggest an 11.8% decrease from 2015 to 2035. IEA (2016a) projections, which include the United States and Canada, show emissions levels rising by 10.5% between 2014 and 2030. This comparison identifies a wider range of future energy-related carbon emissions for North America than the national projections, suggesting a large range of predicted futures. Even at the aggregate “Low emissions” projection scenario, however, the region will not be able to meet the INDC and NDC commitments by 2040 (see Shahiduzzaman and Layton 2017).

Figure 3.11: North American Energy System Carbon Emissions Scenarios in Teragrams (Tg)

Table 3.5. Projected Greenhouse Gas Emissions for North America (2015 to 2040)a

| Economy | 2015 (Tg C)b |

2040 Reference Scenario (Range, Tg C)b |

2015 to 2040 Percent Change in Reference Scenario (Range, Tg C)b |

|---|---|---|---|

| Canada (2015 to 2030) | 173 | 180 (168 to 193) | 3.6 (–3.6 to +10.8) |

| Mexico (2014 to 2040) | 118 | 124 (78 to 140) | 5.6 (–33.9 to +19.0) |

| United States (2015 to 2040) | 1,434 | 1,330 (1,259 to 1,445) | –7.2 (–12.2 to +0.7) |

| North America | 1,725 | 1,634 (1,504 to 1,777) | –5.3 (–12.8 to +3.0) |

Notes

a Sources: EIA 2017k; ECCC 2016c; IEA 2016b.

b Tg C, teragrams of carbon.

3.8.2 Exploratory Energy and Carbon Emissions Scenarios

Exploratory scenarios sketch plausible futures, showing the implications of change in external drivers (Börjeson et al., 2006). Though not necessarily for prediction, they focus on what may happen, ultimately exploring uncertainty in driving forces (Börjeson et al., 2006; Shearer 2005; van der Heijden 2000). Typically, a set of scenarios are constructed to span a wide scope of plausible developments over a very long time span (Jefferson 2015).

The goals of exploratory scenario development include awareness raising of potential challenges, given a wide range of policies and outcomes, and deep insight into societal process interactions and influences (Peterson et al., 2003). In an exploratory scenario exercise, the process of creating the scenarios is often as important as the product (van Notten et al., 2003). Exploratory scenarios address the question of what can happen in the future (Quist 2013). Besides providing a range of outcomes, from both well-understood and not so well-understood changes in conditions, exploratory scenarios have been found useful in accounting for important, but low-probability, condition changes. A criticism of exploratory scenarios is that, while they can demonstrate what might be possible, they are less useful in demonstrating how to achieve a desirable outcome (Robinson 1990).

Well-known examples of exploratory energy scenarios are those initially developed by Royal Dutch Shell and by the World Energy Council. The latest round of Royal Dutch Shell scenarios, titled New Lens Scenarios: A Shift in Perspective for a World in Transition (Royal Dutch Shell 2013), propose multiple lenses through which to view the future. The two pathways in the scenarios are called “Mountains” and “Oceans.” These pathways are defined by different approaches to three key contemporary paradoxes (i.e., prosperity, connectivity, and leadership) and by how societies navigate the tensions inherent in each of these paradoxes. The “Mountains” pathway includes a world locked in status quo, tightly held in place by the currently influential powers. The rigid structure defined by the pathway is created by the demand for energy stability, which results in the steady unlocking of resources, but which also dampens economic dynamism and stifles social mobility. In the “Mountains” pathway, with the global energy supply remaining largely dominated by oil, natural gas, and coal, the world overshoots the 2°C trajectory. During the second half of the century there remain opportunities for CCS technologies and zero-CO2 electricity, but only if mandates promote policies for managing net global emissions.

The “Oceans” pathway, on the other hand, defines a world where power is devolved among competing interests and compromise is necessary. Economic productivity surges with waves of reforms, but social cohesion is sometimes eroded, resulting in political destabilization. In this pathway, market forces have greater prominence over governmental policies. In “Oceans,” biomass and hydrogen play linchpin roles in energy systems by 2100, as oil, natural gas, and coal account for less than 25% of the world’s energy supply, while solar, wind, and biofuels account for about 55%. Because of higher energy use, however, cumulative CO2 emissions are 25% higher in “Oceans” than in “Mountains,” and also, as in the “Mountains” pathway, global CO2 emissions exceed the 2°C threshold. Thus, one of this study’s key findings is that accelerated proactive and integrated policy implementation is necessary to avoid overshooting 2°C of globally averaged warming.

The World Energy Council (2016b) produced world energy scenarios to explore what the council called the “grand transition,” which was emerging from underlying drivers that are reshaping energy economics. The outline of this transition is based on three exploratory scenarios projected to 2050: “Modern Jazz,” “Unfinished Symphony,” and “Hard Rock.” The “Modern Jazz” scenario represents a digitally disrupted, innovative and market-driven world. “Unfinished Symphony” defines a future where intelligent and sustainable economic growth models emerge as the world moves to a low-carbon future. The “Hard Rock” scenario imagines a world of weaker and unsustainable economic growth with inward-looking national policies. Similar to the work of Royal Dutch Shell, mentioned previously, a key finding from the council’s work is that limiting global warming to an increase of no more than 2°C will require an exceptional and enduring policy effort, far beyond already-pledged commitments and with very high carbon prices.

There also have been recent exploratory scenarios developed specifically for economies in North America. The Pew Center on Global Climate Change (Pew; Mintzer et al., 2003) and an Energy Modeling Forum (EMF) study (Clarke et al., 2014; Fawcett et al., 2014a), for example, explore plausible futures for the U.S. energy system. The Pew study describes three divergent paths for U.S. energy supply and use from 2000 to 2035. The creators argue that taken together, these scenarios identify key technologies, important energy policy decisions, and strategic investment choices that could enhance energy security, environmental protection, and economic development over a range of possible futures. The first Pew scenario, called “Awash in oil and gas,” describes a future of abundant supplies of oil and natural gas that are available to consumers at low prices. In this scenario, energy consumption rises and conventional technologies dominate the energy sector. This low–energy price pathway provides few incentives to improve energy efficiency and little concern for energy use. Carbon emissions rise 50% above the 2000 level by 2035. Pew calls the second scenario “Technology triumphs,” which describes a future with a large, diverse set of drivers, converging to accelerate successful commercialization in the U.S. market of many technologies that improve energy efficiency and produce lower carbon emissions. U.S. companies play a key role in the subsequent development of an international market for these technologies. Sustained economic growth and increases in energy consumption are accompanied by a 15% rise in carbon emissions from 2000 levels by 2035. Finally, in Pew’s “Turbulent world” scenario, U.S. energy markets are repeatedly battered by unsettling effects on energy prices and threats to U.S. energy security. High energy prices and uncertainty about energy supplies slow economic growth as the country moves from one technological solution to another, all of which have serious flaws, until finally settling on a program to accelerate the commercialization of hydrogen and fuel cells. Despite slower economic growth than in the other scenarios, carbon emissions still rise 20% above the 2000 level by 2035.

Climate change policy was deliberately excluded from the three Pew base case scenarios. To explore how these policies might affect outcomes, the project provided a climate policy overlay (described as a freeze on CO2 emissions in 2010) and subsequent 2% per year decreases from 2010 to 2025, followed by 3% per year decreases from 2026 to 2035 for each scenario set to achieve the targeted emissions-reduction trajectory of at least 70% from 2000 levels by the end of the century. The portfolio of policies included 1) performance-based energy and emissions standards; 2) incentives to accelerate research and development into low-carbon technologies; 3) a downstream carbon emissions allowance cap-and-trade program applied to electricity generation, the industrial sector, and investment; 4) PTCs for efficiency improvements in energy and emissions technologies; and 5) “barrier busting” programs designed to reduce market imperfections and promote economically efficient decision making (for more details, see Mintzer et al., 2003). When the postulated policy overlay is applied to each base case scenario, it modifies the pattern of energy technology development and future emissions levels. In the “Awash in oil and gas” scenario, the policy overlay results in the highest costs to the economy to meet the carbon constraints with much more stringent policies than in the other scenarios. In the “Technology triumphs” scenario, the policy overlays reinforce the driving forces of the case and accelerate the commercialization of key technologies. In this case, climate policy is uncontroversial, and the United States becomes an international competitor in the development of next-generation energy supply and end-use technologies. In the “Turbulent world” scenario, the imposition of a carbon emissions constraint leads to significant reductions in oil demand and CO2 emissions, decreases based on the emergence of new technologies that sweep the market in transportation and electricity production. All these cases demonstrate the possibility of meeting the goal of a 2°C carbon-reduction trajectory.

EMF is a structured forum for discussing issues in energy and the environment established in 1976 at Stanford University. EMF works through a series of working groups that focus on particular market or policy decisions. The EMF Model Intercomparison Project (MIP) number 24 (EMF24) was designed to compare economy-wide, market-based, and sectoral regulatory approaches of potential U.S. climate policy (Fawcett et al., 2014a).

The EMF24 project focused on policy-relevant analytics that engaged “what if” scenario analysis on the role of technology and scope of regulatory approaches. The effort used nine models to assess the implications of technological improvements and technological availability for three scenarios: no emissions reductions (reference scenario), reducing U.S. GHG emissions 50% by 2050, and reducing U.S. GHGs 80% by 2050. The general technological assumptions include 1) an optimistic CCS or nuclear set of technology assumptions, which have pessimistic assumptions about renewable energy, and 2) an optimistic renewable energy set of technology assumptions for bioenergy, wind, and solar that do not allow CCS and phase out nuclear power energy (see Table 3.6). The EMF24 scenarios allowed banking so that while cumulative emissions were consistent with an emissions cap that followed a linear path to 50% or 80% reductions (relative to 2005 levels) in 2050, actual modeled emissions could be higher. Reference scenarios did not include policies and served as counterfactual starting points for policy application. The policy assumptions explore these seven types of scenarios: 1) “Baseline with no policy,” 2) “Cap-and-trade of varying stringency (0% to 80%),” 3) “Combined electricity and transportation regulatory,” 4) “Electricity and transportation-sector policy combined with a cap-and-trade policy,” 5) “Isolated transportation sector policy,” 6) “Isolated electricity sector policy with a renewable portfolio standard (RPS),” and 7) “Isolated electricity sector policy with a clean energy standard (CES).”

Table 3.6. Technological Assumptions in the Energy Modeling Forum Studya

| Technology | Optimistic Technology | Pessimistic Technology |

|---|---|---|

| End-use energy | End-use assumptions that lead to a 20% decrease in final energy consumption in 2050 relative to the pessimistic technology, no-policy case. | Evolutionary progress. Precise assumptions specified by individual modeling teams. |

| Carbon capture and storage (CCS) | CCS is available. Cost and performance assumptions specified by individual modeling teams. | No implementation of CCS. |

| Nuclear | Nuclear is fully available. Cost and performance specified by each modeling team. | Nuclear is phased out after 2010. No new construction of plants beyond those under construction or planned. Total plant lifetime limited to 60 years. |

| Wind and solar energy | Plausibly optimistic technology development. Cost and performance assumptions specified by individual modeling teams. | Evolutionary technology development. Cost and performance assumptions specified by individual modeling teams. |

| Bioenergy | Plausibly optimistic level of sustainable supply. Supply assumptions specified by individual modeling teams. | Evolutionary technology development representing the lower end of sustainable supply. Supply assumptions specified by individual modeling teams. |

Notes

a Source: Clarke et al., 2014.

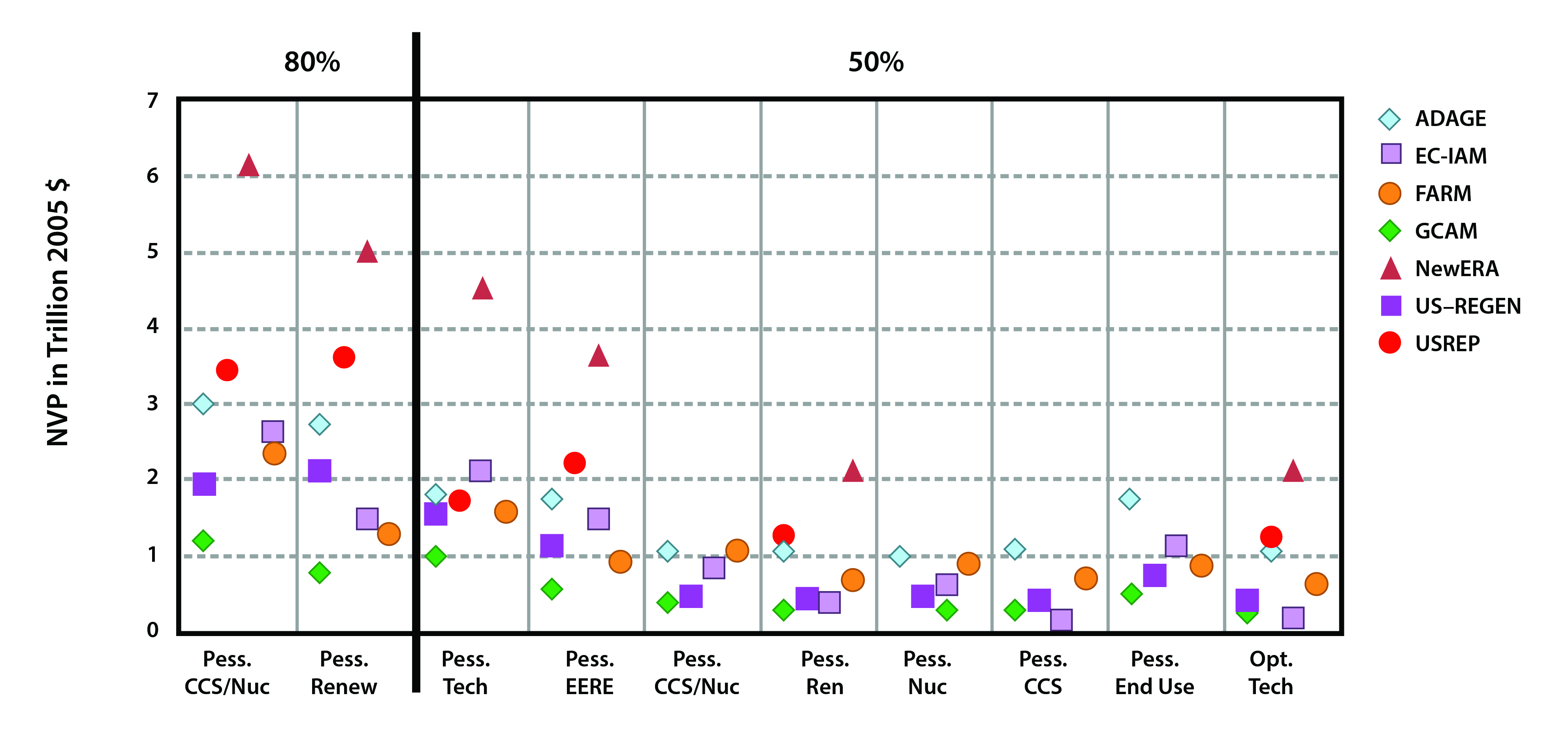

The study finds that even under the most optimistic technology assumptions, no reference scenario among the different models meets the mitigation goals of 50% by 2050. The greatest average annual emissions reduction identified across models was 0.19% per year through 2050. Alternatively, every model could meet 50% reduction scenarios even under the most pessimistic assumptions about technology and produce the 80% reduction scenarios without nuclear and CCS, relying exclusively on renewable energy and end-use measures under different policy assumptions (Clarke et al., 2014). As in all other studies mentioned thus far, the EMF24 project confirms that mitigation at the 50% or 80% level will require a dramatic transformation of the energy system over the next 40 years.

Estimates from the EMF24 study indicate that the total mitigation costs of achieving 80% emissions reductions fall between $1 trillion and $4 trillion (US$ 2005) for most of the 80% emissions reduction scenarios through 2050, although one outlying model found costs as high as $6 trillion (US$ 2005) (Clarke et al., 2014; see Figure 3.12). In the EMF24 study, not all models were able to report the same cost metrics due to structural differences, so the costs reported for each model reflect different ways of handling, such as the value of leisure time and costs associated with reduced service demands. A thorough description of the differences among these metrics can be found in Fawcett et al. (2014a).

Figure 3.12: Net Present Value of Mitigation Costs from 2010 to 2050 from Seven Different Models

Taken together, the Pew and EMF24 U.S. scenario analyses reveal three important conclusions: 1) the cumulative costs of mitigation for achieving an 80% emissions reduction (relative to 2005 levels) by 2050 fall between $1 trillion and $4 trillion (US$ 2005); 2) investment decisions today, especially those that support key technologies, will have a significant impact on North American energy-related carbon emissions tomorrow; and 3) a portfolio of policies combining technology performance targets, market incentives, and price-oriented measures can help the United States meet complementary energy security and climate protection goals.

In summary, the differing exploratory scenarios provide a wide range of futures. All emphasize the importance of policy and technology development in guiding the world (see also IEA 2017c) and North America into a future of stable economic growth, global energy security, and reduced emissions. The finding that significant future emissions reductions require policy is further supported by the work of Shahiduzzaman and Layton (2017), who suggest that for the United States to achieve the 2025 target emissions levels, which are in line with the 2°C future world, the combined average annual mitigating contribution from energy efficiency, carbon intensity, and energy improvements will need to be at least 33% higher and as much as 42% higher than current trends portend, depending on the level of structure change in the U.S. economy.

3.8.3 Energy and Carbon Emissions Backcasting Scenarios

The third type of scenario includes normative, transformation studies. Typically, these scenarios start with the end state and work backwards, hence the name “backcasting” (Lovins 1977; Robinson 1982). Backcasting can be implemented in a large variety of ways (Quist 2007; Quist et al., 2011), although methods typically involve two steps: 1) development of desirable images of the future (visions) and 2) backwards analysis of how these visions can be realized (Höjer and Mattsson 2000; Quist 2013; Robinson 1988). Among the many advantages of employing backcasting is its capability to calculate the cost of investments, such as energy infrastructure, necessary to achieve the visionary future. Backcasting scenarios address the question, what would need to happen to achieve a specific end state? (Quist 2013).

A number of new backcasting studies examine “deep decarbonization” futures, which refer to the reduction of GHG emissions over time to a level consistent with limiting global warming to 2°C or less. There is extensive development of global-scale energy-environment modeling for this purpose (for a brief review, see Fawcett et al., 2014b). More recently, a body of literature also has emerged on scenario pathways consistent with a 1.5°C world (Kriegler et al., 2018; Millar et al., 2017; Rogelj et al., 2015, 2018; Su et al., 2017). There also are a significant number of studies arguing that it is possible for the United States, and the world, to significantly reduce carbon emissions by 2050 (Delucchi and Jacobson 2011; Fthenakis et al., 2009; IPCC 2011; Jacobson and Delucchi 2011; Jacobson et al., 2015; MacDonald et al., 2016; NREL 2012; Mai et al., 2014).16 This chapter focuses on a select number of studies in North American economies with visions of a 2°C future using multiple technologies. These scenarios include those from 1) the Deep Decarbonization Pathways Project (2015; DDPP); and 2) the White House (2016) Mid-Century Strategy report.

The DDPP is a collaborative global initiative of the United Nations Sustainable Development Solutions Network (UNSDSN) and Institute for Sustainable Development and International Relations (IDDRI). Each of the 16 countries participating in the project explores how an individual nation can transform its energy systems by 2050 to limit the anthropogenic increase in global mean surface temperature to less than 2°C. Deep decarbonization pathways focus on a wide range of important actions, although three appear most important to the energy system: 1) high energy efficiencies across all sectors; 2) electrification wherever possible, with nearly complete decarbonization of the electricity system; and 3) reduced carbon in other kinds of fuels (Deep Decarbonization Pathways Project 2015). Included in this review are scenarios from Canada, Mexico, and the United States, each of which is engaged in its own scenario exercises and that are not official governmental exercises.

The Canadian DDPP examines major shifts in technology adoption, energy use, and economic structure that are consistent with continued economic and population growth and a nearly 90% reduction in national GHG emissions from 2010 levels by 2050 (Bataille et al., 2014, 2015). In the reference case, national emissions are relatively stable over the forecast period, reaching 201 Tg C in 2050 (181.6 Tg C of energy emissions) with the net impact of higher oil prices and a production increase of 13 Tg C (7%) by 2050. The Canadian deep decarbonization pathway achieves an overall GHG emissions reduction of nearly 90% (178 Tg C) from 2010 levels by 2050, while maintaining strong economic growth. Over this period, GDP rises from $1.26 trillion to $3.81 trillion (US$ 2010), a tripling of Canada’s economy. The reduction in emissions is driven most significantly by a reduction in the carbon intensity of energy use, as renewables and biomass become the dominant energy sources and there is broad fuel switching across the economy toward electricity and biofuels. Electricity production nearly completely decarbonizes. Overall, the carbon intensity of Canada’s total primary energy supply declines by 90% between 2010 and 2050. This result is robust across different technology scenarios. For example, if biofuels are not viable, transportation could transition to increased use of electricity generated with renewables and fossil fuels with CCS, especially if better batteries become available. If CCS processes are not available, the electricity sector could decarbonize using more renewables and nuclear. End-use energy consumption rises by only 17% over this period, compared to a 203% increase in GDP. This difference is due both to structural changes in the economy and to increases in energy efficiency.

The costs of these transformations include significant restructuring of energy investments. The study found that overall incremental investment increases by around $13.2 billion (CAD$ 2014) annually (8% increase relative to historic levels), but this average increase hides sectoral differences. Consumers spend $3.0 billion (CAD$ 2014) less each year on durable goods like refrigerators, cars, appliances, and houses, while firms must spend $16.2 billion (CAD$ 2014) more. Approximately $13.5 billion (CAD$ 2014) of costs are in the electricity sector (+89% over historical levels), by far the most important shift, and $2.9 billion (CAD$ 2014) are in the fossil fuel extraction sector for the adoption of advanced low-emissions technologies such as CCS, solvent extraction, and direct-contact steam generation (+6% over historical levels) (Bataille et al., 2015).

For Mexico, the future analysis was to provide preliminary deep decarbonization routes to determine whether there are general conclusions that can be drawn at an aggregate level. The scenarios sought economic development that is low–carbon, rather than unconditional decarbonization. Therefore, Mexico’s deep decarbonization project aimed to reduce GHG emissions to 50% below 2000 levels by 2050 (a target of approximately 71 Tg C), in accordance with the target set by the General Climate Change Law of 2012. The reference scenario used by the project, based on current trends and well-informed assumptions of future activity for the main drivers of CO2 emissions, predicted emissions could reach 246 Tg C by 2050. The central deep decarbonization scenario suggests that total CO2 emissions could reach 68.2 Tg C by 2050, including fugitive and process emissions (a 51% decline from 2000 levels), largely induced by declines in energy intensity of 59% and declines in CO2 intensity of 66%. Final energy consumption in 2050 reaches 8.1 EJ, 35% less than in the reference trajectory, although it is an increase of 38% compared with the 2010 levels of 5.9 EJ. Costs of the transformation were not calculated. These reductions were plausible under certain assumptions, such as accelerated increases in energy-efficiency uptake across all sectors; rapid development and deployment of CCS; zero-emissions vehicles; energy-storage technologies; smart transmission and distribution (smart grids); and system flexibility to promote, adopt, and combine diverse options over the time frame of decarbonization (Tovilla and Buira 2015[eds.]).

For the U.S. DDPP, the vision is to achieve an 80% GHG reduction below 1990 levels by 2050, and DDPP uses multiple pathways to achieve these reductions through existing commercial or near-commercial technologies (Williams et al., 2014, 2015). The three pillars of decarbonization across all pathways are high-efficiency end use of energy in buildings, transportation, and industry; nearly complete decarbonization of electricity; and reduced carbon in fuels and electricity production. Pathways were named “High renewables,” “High nuclear,” “High carbon capture and storage,” and “Mixed,” based on the dominant strategy used for energy generation and carbon mitigation. The goal of the pathways was to reduce total GHG emissions from a net of around 1,470 Tg C and energy emissions of 1,390 Tg C to overall net GHG emissions of no more than 300 Tg C and fossil fuel combustion emissions of no more than 205 Tg C. To achieve this outcome, the vision includes a reduction of petroleum consumption by 76% to 91% by 2050 across all scenarios. The study finds that all scenarios met the target, demonstrating robustness by showing the existence of redundant technology pathways to deep decarbonization.

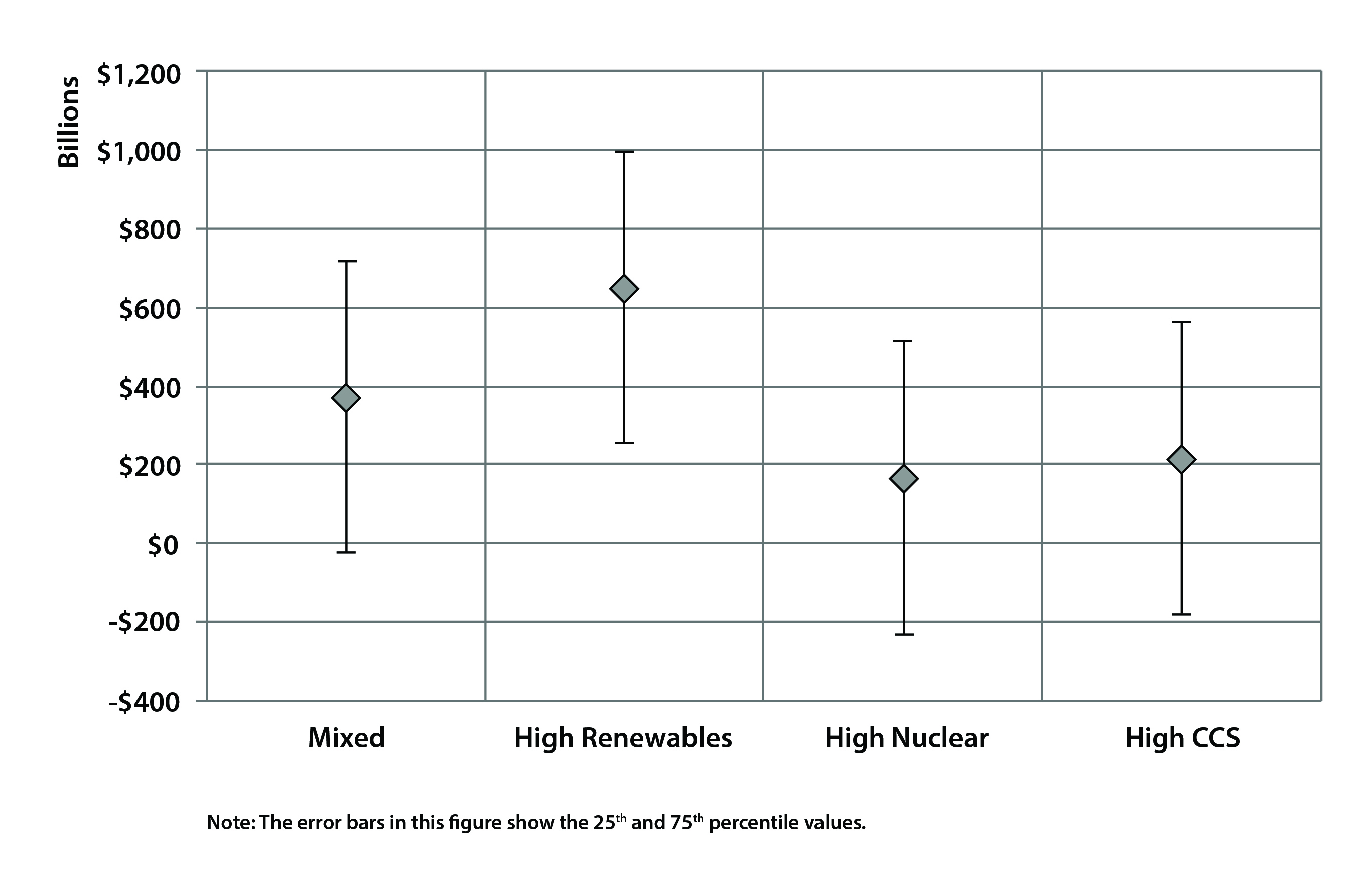

The costs of the transformation include incremental energy system costs (i.e., incremental capital costs plus net energy costs). These are defined by costs of producing, distributing, and consuming energy in a decarbonized energy system relative to that of a reference case system based on the EIA (2013c) report as a metric to assess the costs of deep reductions in energy-related CO2 emissions. Based on an uncertainty analysis of key cost parameters in the four analyzed cases, the 25% to 75% range extends from negative $90 billion to $730 billion (US$ 2012) in 2050 (see Figure 3.13). The median costs value is just over $300 billion (US$ 2012). This median estimate of net energy system costs is 0.8% of U.S. GDP in 2050, with a 50% probability of costs falling between –0.2% and 1.8% of GDP. Uncertainty in costs is due to assumptions about consumption levels, technology costs, and fossil fuel prices nearly 40 years into the future. The higher end of the probability distribution (75% estimate of $730 billion) assumes little to no technology innovation over the next four decades. The overall costs of deeply decarbonizing the energy system is dominated by the incremental capital cost of low-carbon technologies in power generation, light- and heavy-duty vehicles, building the energy system, and industrial equipment. The U.S. DDPP result of total mitigation costs of $1 trillion to $2 trillion through 2050 is consistent with the EMF24 study (Williams et al., 2015).

Figure 3.13: Incremental Energy System Costs in 2050

The report suggests that the transition to a deeply decarbonized society would not require major changes in individual energy use because the scenarios were developed to support the same level of energy services and economic growth as the references case of EIA (2013c). For example, Americans would not be required to use bicycles in lieu of cars, eat purely vegetarian diets, or wear sweaters to reduce home heating loads (Williams et al., 2015).

The aforementioned White House (2016) Mid-Century Strategy (MCS) report charts pathways for the United States consistent with a reduction of 80% or more (relative to 2005 levels) by 2050. The MCS goal reduces annual emissions from around 1,609 Tg C in 2005 to 410 Tg C in 2050. The ensemble of scenarios used differs in regard to the reliance on key low-carbon technologies and decarbonization strategies. Three sets of MCS scenarios are 1) “MCS benchmark,” which assumes continued innovation spurred by decarbonization policies and current levels of RD&D funding; 2) “Negative emissions,” two alternative scenarios that explore the implications of achieving different levels of negative emissions such as no CO2 removal technology and limited sink scenarios; and 3) “Energy technology,” which comprises three scenarios that explore challenges and opportunities associated with the low-carbon energy transition: no CCS, smart growth, and limited biomass scenarios.

The study findings suggest that by 2050 energy efficiency can reduce primary energy use by over 20% from 2005 levels and that nearly all fossil fuel electricity production can be replaced by low-carbon technologies, including renewables, nuclear, and fossil fuels or bioenergy combined with CCS. Furthermore, the study argues that there are opportunities to expand electrification into the transportation, industrial, and buildings sectors, reducing their direct fossil fuel use by 63%, 55%, and 58%, respectively, from 2005 to 2050. Reaching the MCS goal requires a substantial shift in resources away from GHG-intensive activities, including increasing annual average investments in electricity-generating capacity to between 0.4% and 0.6% of U.S. GDP.

In summary, the backcasting exercises for North America and the United States suggest that reaching a goal of 80% reductions in GHG emissions (relative to 2005 levels) is plausible, although achieving the goal will require both policies and technological advances. The incremental cost of mitigation for the United States was identified as between 0.4% to 0.8% of annual GDP (Williams et al., 2014) and an annual incremental cost of $13.2 billion (CAD$ 2014) for Canada. The final numbers are comparable with the $1.5 trillion to $2.0 trillion costs identified by the Edison Electric Institute (2008) for infrastructure investments necessary to 2030 for upgrading the electricity system.

There are significant caveats to these results. Previously mentioned mitigation costs do not include direct benefits (e.g., avoidance of infrastructure damage) and co-benefits (e.g., avoided human health impacts from air pollution) of emissions reductions. These benefits and co-benefits can be substantial. For example, U.S. EPA (2015a, 2017b) estimated some of the benefits and co-benefits of climate mitigation through 2100 for the United States. In their most recent report (U.S. EPA 2017b), the agency examined 22 issue areas across the human health, infrastructure, electricity, water resources, agriculture, and ecosystems sectors. Annual cost estimates for these sectors due to climate change during the year 2050 were $170 billion and $206 billion (US$ 2015) under Representative Concentration Pathway (RCP) 4.5 and RCP8.5 conditions, respectively. By 2100, costs in these sectors due to climate change were estimated at $356 billion and $513 billion annually (US$ 2015) under RCP4.5 and RCP8.5 conditions, respectively (U.S. EPA 2017a).

The benefits and co-benefits of mitigation may be even larger than estimated. U.S. EPA (2017b) noted that its report estimates did not include some health effects (e.g., mortality due to extreme events other than heat waves, food safety and nutrition, and mental health and behavioral outcomes); effects on ecosystems (e.g., changes in marine fisheries, impacts on specialty crops and livestock, and species migration and distribution); and social impacts (e.g., national security and violence). Other estimates at the global scale, include damages (in terms of reduced consumption) from business-as-usual scenarios (resulting in up to a 4°C warming by 2100) that range from 1% to 5% of the global GDP, incurred every year (Norhaus 2013). Costs may be even higher if temperatures continue to rise, with potential reductions of 23% of global incomes and widening global income inequality by 2100 (Burke et al., 2015a).

Additionally, the costs to mitigate may be lower than reported depending on when they appear. For example, in some studies, the majority of energy mitigation costs are incurred after 2030, as deployment of low-carbon infrastructure expands. Technology improvements and market transformation over the next decades, however, could significantly reduce these expected costs. Also important, as mentioned previously in this report, is that CO2 removal technologies such as CCS; carbon capture, utilization, and storage (CCUS); and BECCS are not currently deployed at scale, as many of the listed scenarios mentioned. Nuclear power expansion, as envisioned in some scenarios, also faces technical and political challenges (see Box 3.2, Potential for Nuclear Power in North America).

The changing climate also may affect energy supply and use in a variety of ways, and adapting to these changes will create future North American energy systems that differ from those of today in uncertain ways (Dell et al., 2014). While the trajectories from the outlined scenarios are “plausible,” whether any of them are “feasible” depends on a number of subjective assessments such as whether Canada, Mexico, and the United States at this time or any time in the future would be willing to make the necessary transformations and how future climate change will transform both opportunities and risks (Clarke et al., 2014; Dell et al., 2014).

See Full Chapter & References